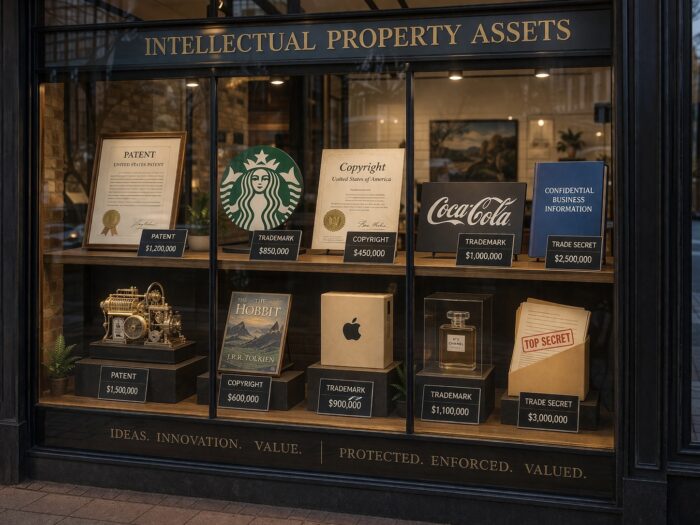

In today’s knowledge-based economy, businesses must understand the value of intellectual property (IP). Intellectual property plays a central role in how businesses create and protect their value. Intellectual property refers to intangible assets that are legally protected, including patents, trademarks, copyrights, and trade secrets. IP is capable of generating substantial economic benefits. These intellectual property assets often represent a significant portion of a company’s overall business value. Thus, understanding the economic value of IP assets is critical for informed business strategy.

Moreover, valuing IP assets is required across a range of financial processes, including financial reporting, tax planning, and dispute resolution. Well-executed intellectual property management and valuation enables businesses to maximize the value of their IP assets and align their IP protection strategies with long-term success.

Intellectual property is legally protected, transferable, and capable of generating economic benefits and monetary value. Common forms of intellectual property rights include patents, trademarks, copyrights, and trade secrets, each of which can be owned, licensed, enforced, or incorporated into a company’s business model.

Under the Patent Act, a patent confers “the right to exclude others from making, using, offering for sale, or selling” the claimed invention under 35 U.S.C. § 154, thereby creating a legally enforceable exclusivity that drives future economic benefits and competitive advantage. Patents are also expressly treated as personal property that can be assigned or licensed, reinforcing their status as valuable IP assets within broader business assets. See 35 U.S.C. § 261.

Similarly, copyright law grants a bundle of exclusive rights, including reproduction, distribution, and public display under 17 U.S.C. § 106, that allow the owner to control and monetize creative works, forming the basis for future cash flows and licensing revenue. These exclusive rights make copyrights a central category of intellectual property assets with measurable economic value.

Trademark rights, governed primarily by the Lanham Act, protect brand identifiers such as names, logos, and slogans that distinguish goods or services in commerce. Federal trademark registration provides nationwide priority and evidentiary advantages, including prima facie evidence of validity and ownership under 15 U.S.C. § 1057(b). These rights enable a business to prevent confusingly similar uses under 15 U.S.C. § 1114, preserve goodwill, and maintain brand-driven future revenue potential, making trademarks particularly valuable intellectual property assets tied to customer recognition.

For trade secrets, the Defend Trade Secrets Act defines protectable information as that which “derives independent economic value… from not being generally known” and is subject to reasonable efforts to maintain secrecy under 18 U.S.C. § 1839(3). The statute also provides a federal civil cause of action for misappropriation under 18 U.S.C. § 1836, reinforcing that secrecy itself can create substantial IP value when it preserves a competitive advantage.

IP assets essentially derive their value from their intrinsic value (e.g., the improvements provided by an invention, the market value of a copyrighted work, etc.) in combination with the statutory framework that prevents others from using the IP asset. The legal rights provided by the statutory framework allow the owner of the IP asset to exclude competitors, and the capacity to produce future benefits through commercialization, licensing, or strategic deployment within a company’s operations.

IP assets can be independently identified, transferred, and monetized through structured commercial arrangements. IP can be licensed, sold, or pledged as collateral, enabling businesses to unlock economic benefits and create additional income streams. Moreover, strong IP portfolios may serve as signals of reduced risk and future revenue potential in financing and M&A contexts. Valuing intellectual property helps establish enhanced market value, collateral, and accurate financial assessments of a business.

Registered IP rights strengthen IP protection, reduce copying risk, and support economic growth because they provide legally enforceable exclusivity grounded in statute. For example, patents confer a right to exclude others from making, using, or selling the claimed invention under 35 U.S.C. § 154, while trademark registrations under 15 U.S.C. § 1057 provide nationwide priority and evidentiary presumptions of validity and ownership. Copyright law similarly grants exclusive rights to reproduce and distribute protected works under 17 U.S.C. § 106, and trade secrets are protected so long as they derive independent economic value from not being generally known under 18 U.S.C. § 1839(3). These intellectual property assets therefore provide the legal power to prevent third parties from using or exploiting protected subject matter, preserving future economic benefits and reinforcing a company’s competitive advantage. At the same time, because IP rights are enforceable in court and transferable, courts and regulators routinely require reliable intellectual property valuation methodologies to quantify their monetary value in disputes, transactions, and reporting contexts.

In the legal dispute context, courts often rely on the hypothetical negotiation framework set forth in Georgia-Pacific Corp. v. U.S. Plywood Corp., 318 F. Supp. 1116 (S.D.N.Y. 1970), which remains a foundational approach for determining reasonable royalty damages in patent litigation. This framework incorporates detailed financial analysis of expected future cash flows, established licensing practices, and comparable agreements to estimate the present value of the use of the IP. Similar reasoning applies in copyright litigation cases, where damages may include the fair market value of a license under 17 U.S.C. § 504. In trade secret litigation cases, courts may award a reasonable royalty based on the value of the misappropriated information. See University Computing Co. v. Lykes-Youngstown Corp., 504 F.2d 518 (5th Cir. 1974). These authorities underscore that valuing intellectual property in litigation is inherently tied to estimating the economic value of the rights at issue using recognized IP valuation methods.

Transfers of IP assets also have significant tax implications. For example, related entities that transfer intellectual property assets between them must determine objective arm’s-length pricing for those intangible transfers. These rules require the use of reliable valuation methods, often grounded in the income approach, market method, or other accepted financial processes, to ensure that intercompany transactions reflect what unrelated parties would have agreed to under comparable circumstances. Consequently, intellectual property valuation is integral to financial management, tax compliance, and broader business strategy, and must be carefully considered in the internal management of the business to properly account for IP assets, support financial statements, and avoid regulatory exposure.

IP value rises when legal protections are broad, durable, and enforceable, because those protections are what allow an owner to exclude competitors and capture economic benefits from intellectual property assets. For patents, the statutory right to exclude under 35 U.S.C. § 154, coupled with infringement liability under 35 U.S.C. § 271, directly underpins the ability of a patent holder to control use and monetize the invention over its remaining term, making scope, validity, and duration central to future revenue potential and future benefits.

Under the Lanham Act, federal trademark registration provides significant evidentiary advantages, and it can serve as conclusive evidence of validity and exclusive right to use in commerce, reinforcing brand-based competitive advantage and preventing damage to a brand.

Copyright law similarly grants exclusive rights to reproduce, distribute, and display works under 17 U.S.C. § 106, but enforcement generally requires copyright registration for U.S. works, making registration a practical prerequisite to realizing the monetary value of those rights. See 17 U.S.C. § 411. In Fourth Estate Pub. Benefit Corp. v. Wall-Street.com, LLC, 586 U.S. 296 (2019), the Supreme Court confirmed that registration, not merely application, is required before suit.

For trade secrets, the Defend Trade Secrets Act defines protectable information as that which derives independent economic value from not being generally known and is subject to reasonable efforts to maintain secrecy under 18 U.S.C. § 1839(3). This statutory definition ties economic value directly to secrecy itself, if confidentiality is lost, so too is the asset’s value. Courts consistently emphasize this connection, recognizing that the value of a trade secret lies in its ability to provide a competitive advantage through exclusivity.

More broadly, these legal frameworks allow intellectual property rights to be enforced in court, enabling licensing, assignment, and other commercial arrangements based on exclusivity. As a result, the strength, scope, and enforceability of those rights directly influence whether an IP owner can extract economic value, gain market advantage, and ultimately realize the full value of intellectual property over time. Intellectual property creates value in a business through these legal mechanisms.

Intellectual property valuation is the process of determining the monetary value of intellectual property assets based on their ability to generate future economic benefits, such as future cash flows, licensing revenue, or strategic competitive advantage. For business owners, valuing IP assets is essential for financial reporting, negotiating licensing deals, securing financing, supporting mergers and acquisitions, and guiding internal management decisions about how to deploy and protect IP rights.

The valuation process requires gathering information about the asset’s legal strength, market demand, commercial use, and role in the company’s business model, along with broader financial analysis of expected future income and risk. Because intellectual property assets are intangible assets, their quantifiable value must be inferred through structured financial processes rather than direct observation.

The primary methods for valuing intellectual property are the income method, market method, and cost method. The income approach estimates the present value of expected cash flows or royalties attributable to the IP. The market method compares the asset to comparable IP or similar assets in a well-established market, while the cost method considers the historical cost or replacement cost of creating the asset.

Choosing the appropriate valuation method depends on factors such as the valuation date, the asset’s legal protections, availability of market comparables, and the purpose of the valuation: i.e., whether for a transaction, litigation, tax planning, or strategic planning. No single valuation method fits every situation. Accurate IP valuation requires selecting the approach that best captures the asset’s future revenue potential and overall contribution to the company’s assets, ensuring that the resulting valuation reflects real-world economic benefits provided by the company's IP, rather than theoretical assumptions.

The income approach is the most commonly used method for revenue-producing IP assets. It estimates present value from future cash flows, positive cash flows, cost savings, or an expected income stream. This approach makes sense when the asset already helps the company generate revenue or has clear future revenue potential. In licensing and damages settings, determining royalty rates often starts with the hypothetical negotiation framework from the Georgia-Pacific Corp. approach.

The market approach values intellectual property by comparing the subject asset to comparable IP, similar assets, or real-world transactions such as licenses, assignments, or sales in a well established market. This method is grounded in supply-and-demand principles and asks what buyers have actually paid for comparable rights under similar conditions. It is particularly useful for trademarks, software, and other intellectual property based businesses where there is tangible evidence of prior deals, including royalty rates or purchase prices. However, applying the market approach can be challenging because many IP assets have unique or novel characteristics, and reliable public data is often limited. Differences in industry, geography, exclusivity, and field of use can also affect comparability. Despite these limitations, when appropriate comparables exist, the market approach can provide reliable benchmarks and help establish approximate values grounded in real commercial activity.

The cost method is an IP valuation method used when an IP asset essentially lacks a proven income stream. This valuation method estimates the monetary value of intellectual property assets by calculating what it would cost to recreate, replace, or design around the asset, including historical cost, development time, prosecution expense, and technical risk. As part of the broader valuation process, it helps establish approximate values where market data or future cash flows are uncertain. The cost approach is commonly applied to early-stage patents, copyrights, and trade secrets that have not yet demonstrated future economic benefits. However, proper valuation requires recognizing that cost does not always equal fair value. An asset may have low development cost but high economic value, or significant investment but limited economic benefits if it fails to generate revenue.

The valuation process requires gathering license agreements, sales records, margins, market studies, prosecution files, chain-of-title documents, and commercialization evidence. Because IP is less visible than other business assets, proper valuation depends on tangible evidence: contracts, customer demand, renewal history, legal scope, and adoption data. The valuation process also asks what cash flows are actually attributable to the IP, rather than to goodwill, other intangible assets, or ordinary operating functions.

Several factors move the value of intellectual property up or down, including remaining enforceable term, claim scope, validity risk, infringement risk, market size, substitutability, brand strength, and scalability. Licensing history is particularly important, often providing a practical benchmark for determining value and assessing damages. For example, in patent cases royalty expectations must respect legal limits on duration. In Kimble v. Marvel Entertainment, LLC, 576 U.S. 446 (2015), the Court confirmed that royalties generally cannot extend beyond patent expiration, directly impacting discounted cash-flow models and reinforcing that the value of intellectual property is tied to enforceability and duration of rights.

A formal intellectual property valuation is critical whenever a business must determine the fair value or monetary value of its intellectual property assets for strategic, legal, or financial purposes. In practice, IP valuation is most commonly needed before major licensing deals, mergers, acquisitions, fundraising, or other commercial arrangements based on IP, where parties must agree on the economic value of IP assets and projected future cash flows. It is also essential for financial reporting, tax compliance, and other various financial processes.

Beyond transactions, valuing intellectual property is often required in legal disputes, including infringement or damages analyses, where courts expect a proper valuation supported by reliable financial analysis and expert testimony under Federal Rule of Evidence 702 and Daubert v. Merrell Dow Pharmaceuticals, Inc., 509 U.S. 579 (1993). Businesses also rely on accurate IP valuation for internal management, portfolio optimization, and assessing future economic benefits tied to their intellectual property rights.

The value of intellectual property is found in its ability to create revenue, sustain a competitive advantage, and contribute meaningfully to a company’s overall economic value. Intellectual property assets are not merely abstract rights, they are valuable assets that can produce revenue and a competitive advantage in the marketplace. Additionally, IP valuation and analysis can be a key component of business strategy, informing decisions about commercialization, enforcement, and investment in particular IP assets. Businesses that manage their intellectual property assets are better positioned to capitalize on their innovations, mitigate risk, and maximize the long-term value of their intellectual property.

If you need assistance with an intellectual property matter, please contact our office for a consultation.

© 2026 Sierra IP Law, PC. The information provided herein does not constitute legal advice, but merely conveys general information that may be beneficial to the public, and should not be viewed as a substitute for legal consultation in a particular case.

"Mark and William are stellar in the capabilities, work ethic, character, knowledge, responsiveness, and quality of work. Hubby and I are incredibly grateful for them as they've done a phenomenal job working tirelessly over a time span of at least five years on a series of patents for hubby. Grateful that Fresno has such amazing patent attorneys! They're second to none and they never disappoint. Thank you, Mark, William, and your entire team!!"

Linda Guzman

Sierra IP Law, PC - Patents, Trademarks & Copyrights

FRESNO

7030 N. Fruit Ave.

Suite 110

Fresno, CA 93711

(559) 436-3800 | phone

BAKERSFIELD

1925 G. Street

Bakersfield, CA 93301

(661) 200-7724 | phone

SAN LUIS OBISPO

956 Walnut Street, 2nd Floor

San Luis Obispo, CA 93401

(805) 275-0943 | phone

SACRAMENTO

180 Promenade Circle, Suite 300

Sacramento, CA 95834

(916) 209-8525 | phone

MODESTO

1300 10th St., Suite F.

Modesto, CA 95345

(209) 286-0069 | phone

SANTA BARBARA

414 Olive Street

Santa Barbara, CA 93101

(805) 275-0943 | phone

SAN MATEO

1650 Borel Place, Suite 216

San Mateo, CA, CA 94402

(650) 398-1644. | phone

STOCKTON

110 N. San Joaquin St., 2nd Floor

Stockton, CA 95202

(209) 286-0069 | phone

PORTLAND

425 NW 10th Ave., Suite 200

Portland, OR 97209

(503) 343-9983 | phone

TACOMA

1201 Pacific Avenue, Suite 600

Tacoma, WA 98402

(253) 345-1545 | phone

KENNEWICK

1030 N Center Pkwy Suite N196

Kennewick, WA 99336

(509) 255-3442 | phone

2023 Sierra IP Law, PC - Patents, Trademarks & Copyrights - All Rights Reserved - Sitemap Privacy Lawyer Fresno, CA - Trademark Lawyer Modesto CA - Patent Lawyer Bakersfield, CA - Trademark Lawyer Bakersfield, CA - Patent Lawyer San Luis Obispo, CA - Trademark Lawyer San Luis Obispo, CA - Trademark Infringement Lawyer Tacoma WA - Internet Lawyer Bakersfield, CA - Trademark Lawyer Sacramento, CA - Patent Lawyer Sacramento, CA - Trademark Infringement Lawyer Sacrament CA - Patent Lawyer Tacoma WA - Intellectual Property Lawyer Tacoma WA - Trademark lawyer Tacoma WA - Portland Patent Attorney - Santa Barbara Patent Attorney - Santa Barbara Trademark Attorney