What is goodwill in business? Goodwill in the business context is the intangible value of a company that makes it worth more than the fair market value of its identifiable assets minus liabilities. In plain English, goodwill represents the premium paid for a business because of its brand reputation, customer loyalty, customer relationships, market position, and other advantages that do not appear as physical assets on a shelf or in a warehouse. In accounting, goodwill becomes a central consideration when one company buys another. If the company has good consumer recognition and other intangible value that is beyond the company’s net identifiable assets, the premium paid for the acquired company is the value of the goodwill. Under tax regulations, goodwill is tied to the expectancy of continued customer patronage, including reputation and business name value.

Goodwill in accounting is an intangible asset recorded in a business combination when an acquiring company pays a purchase price that exceeds the fair value or fair market value of the acquired business’s identifiable net assets. In other words, goodwill is not assigned to a specific machine, building, contract, copyright asset, patent, or other separately identifiable asset. Instead, goodwill represents the residual value left after the acquiring company identifies and values the acquired company’s assets and liabilities.

The shorthand formula for calculating goodwill is:

Goodwill = Purchase Price - (Fair Market Value of Assets - Fair Market Value of Liabilities).

Because assets minus liabilities equals net assets, goodwill represents the premium paid above the company’s net assets. More precisely, in an acquisition, the buyer first determines the fair value of the target company’s identifiable assets, including tangible assets and separately identifiable intangible assets, and then subtracts the fair value of the target company’s assumed liabilities. The result is the target company’s identifiable net assets. If the buyer pays more than that amount, the excess is recorded as goodwill on the acquiring company’s balance sheet.

Assume Company A acquires Company B for $10 million. Company B has tangible assets worth $6 million, identifiable intangible assets worth $2 million, and liabilities of $1 million. The net identifiable assets are $7 million. If the buyer pays $10 million, the goodwill value is $3 million.

That $3 million of excess value may reflect strong brand reputation, loyal customers, and proprietary systems. In mergers and business acquisitions, goodwill often constitutes a significant portion of the total deal price because goodwill captures the intangible value that makes a business worth more than its tangible assets alone.

Goodwill is an intangible asset, but it differs from other intangible assets. An intangible asset is identifiable when it is separable or arises from legal or contractual rights, such as separably valuable patent. Business goodwill is not recognized as a separate asset because it is not an identifiable thing that can be valuated separately from the business. This accounting treatment is important because goodwill is a residual accounting measure, not a separately traded asset. It appears on the balance sheet only because the acquisition price indicates that the business as a whole is worth more than the current market value of its identifiable assets after liabilities are deducted.

Patents, trademarks, copyrights, trade secrets, domain names, licenses, and some customer contracts can often be separately identified, valued, licensed, or sold. Goodwill cannot be bought or sold independently from the business because it reflects the overall business goodwill, brand equity, customer relationships, operating reputation, and competitive advantage of a going concern.

Business owners often use fair market value to mean what a willing buyer would pay in a fair market transaction. Accounting standards define fair value as the price received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.

That distinction matters. A company’s historical cost may differ from current market value, and the market value of assets may differ from book value on the company’s balance sheet. A buyer assessing business value will consider the present value of future cash flows, similar companies operating in the market, the current market value of assets and liabilities, and the acquired business’s expected net income.

Goodwill has no market for independent trading. Unlike a truck, a building, or a patent, goodwill usually cannot be sold alone. That makes valuing goodwill highly subjective and vulnerable to management over-optimism. A goodwill valuation may depend heavily on forecasts, discount rates, margin assumptions, and the income approach, which estimates the present value of future cash flows.

This is why goodwill is not the same as cash, inventory, or other readily marketable assets. It reflects business value, but it is also a residual accounting number: the premium paid after identifiable assets and liabilities have been valued.

When a company acquires another company, goodwill is recorded as an intangible asset on the acquiring company’s balance sheet, sometimes called the acquirer’s balance sheet, after the purchase price allocation. This increases reported assets and can affect financial metrics such as return on assets and return on equity. High goodwill relative to total assets can be a warning sign. Some investors deduct goodwill from reported assets when evaluating residual equity or tangible book value, especially if they believe management overpaid for acquisitions.

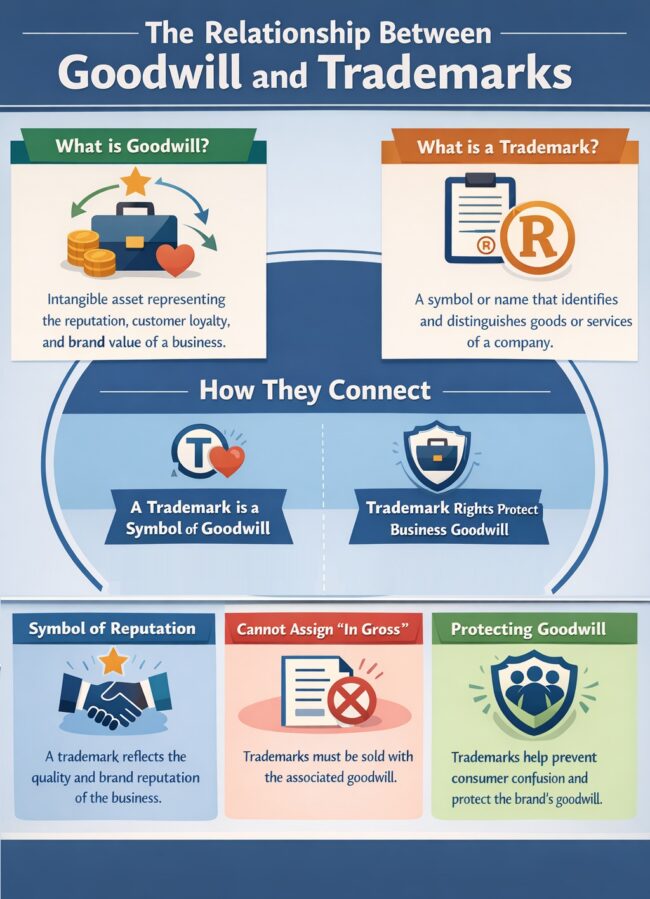

Goodwill is not just an accounting entry or an intangible asset recorded after a business acquisition. In the branding context, business goodwill is the public-facing value of a company’s reputation, customer loyalty, customer relationships, brand equity, and the trust the company previously enjoyed in the marketplace. A trademark is one of the features of that goodwill and a trademark registration is a primary legal tool used to protect that value.

The Lanham Act defines a trademark as any word, name, symbol, device, or combination used to identify and distinguish goods and indicate their source under 15 U.S.C. § 1127. That statutory definition is important because it shows that a trademark’s legal function is not merely decorative. A trademark connects products or services to a particular business source, and that source-identifying function is what allows the mark to carry brand reputation, customer confidence, and goodwill value.

The Supreme Court discussed this relationship in Hanover Star Milling Co. v. Metcalf, 240 U.S. 403 (1916). The dispute involved competing uses of the mark “Tea Rose” for flour. Allen & Wheeler had used the Tea Rose mark for flour as early as 1872 and later transferred its mills, machinery, stock, trademark, and goodwill to a successor corporation. Hanover Star Milling Company, however, had adopted the same Tea Rose mark in good faith in the southeastern United States, without knowledge of Allen & Wheeler’s use, and had built substantial local trade and advertising around the mark. In that southeastern territory, consumers understood “Tea Rose” to mean Hanover’s flour, not Allen & Wheeler’s flour. There was no real confusion between the separate uses of the Tea Rose mark.

The Supreme Court held that the separate use by these two companies was allowable because Hanover adopted the junior use of Tea Rose in good faith without knowledge of Allen and Wheeler's prior use, and there was no consumer confusion between the companies. Moreover, prohibiting Hanover's continued use of the Tea Rose mark would take Hanover’s trade and goodwill and confer it on Allen & Wheeler. This reasoning illustrates that a trademark identifies source of goods and services, and that a trademark is a symbol of the goodwill associated with the source. In other words, trademark law is grounded in protection of the goodwill of a trade or business. Because the junior use of the Tea Rose mark resulted in no confusion or harm to Allen and Wheeler, there was no violation of their trademark rights. A trademark protects the intangible value created when customers associate a name, logo, or brand with a particular company’s products, quality, and reputation. A trademark with no associated goodwill carries no substantial rights.

The Hanover case and many cases thereafter show that trademark rights and goodwill are interdependent. This is why, in an assignment or sale of a trademark, the goodwill value must be included in the transfer of the corresponding trademark.

A trademark is not just a word, logo, slogan, or brand name that can be separated from the business goodwill it represents. Under 15 U.S.C. § 1060(a)(1), a registered mark or pending trademark application is assignable only “with the good will of the business” in which the mark is used, or with the part of the goodwill connected with and symbolized by the mark. The statute also requires assignments to be in writing, and recordation with the USPTO can affect priority against later purchasers.

A trademark assignment divorced from goodwill is often called an assignment “in gross” and may be invalid. The rule exists because a trademark’s function is to identify a consistent commercial source and protect customer expectations. If a buyer acquires only the bare mark, without the customer relationships, brand reputation, product continuity, or business goodwill associated with that mark, consumers may be misled into believing the same business, quality, or source still stands behind the goods or services.

In Marshak v. Green, 746 F.2d 927 (2d Cir. 1984), the Second Circuit applied this principle in the context of a forced sale. David Rick managed and promoted musical groups using the registered trade name “VITO AND THE SALUTATIONS.” Larry Marshak, who held an unsatisfied money judgment against Rick, obtained an order directing the U.S. Marshal to attach and auction Rick’s interest in the trade name. Marshak bought the trade name at auction for $100. The Second Circuit reversed and set aside the sale. The court explained that a trade name or mark has no independent significance apart from the goodwill it symbolizes, and that a sale of a mark divorced from goodwill is an invalid assignment in gross. Because there was no continuity of management, musical quality, or entertainment services, allowing another group to use the name could confuse the public into believing it was seeing the original group associated with that goodwill.

In Premier Dental Products Co. v. Darby Dental Supply Co., 794 F.2d 850 (3d Cir. 1986), the Third Circuit reached the complementary result: an assignment can be valid where the goodwill connected with the mark actually transfers. ESPE, a foreign manufacturer, made IMPREGUM dental impression material. Premier was the exclusive U.S. distributor, had promoted the product in the United States for years, provided seminars and instructions, offered customer support, and was identified in the trade as the domestic source through which IMPREGUM was obtained. ESPE assigned the U.S. IMPREGUM trademark to Premier, together with the goodwill connected with the mark. When Darby Dental imported and sold European-market IMPREGUM products, Premier sued. Darby argued the assignment was essentially a sham because ESPE still manufactured the product. The Third Circuit rejected that argument and held that Premier owned the U.S. trademark because Premier had developed and possessed the domestic goodwill associated with IMPREGUM. The assignment was not merely a transfer of a right to sue, it transferred legal title to the goodwill Premier had used and developed.

Together, Marshak and Premier Dental show why goodwill must travel with a trademark assignment. In Marshak, the attempted sale failed because the buyer acquired only a bare trade name, not the business goodwill, customer recognition, continuity, or service quality that gave the name meaning. In Premier Dental, the assignment was upheld because the assignee already embodied the goodwill symbolized by the mark in the relevant U.S. market. The practical takeaway is that a trademark assignment or business purchase agreement should expressly transfer the goodwill connected with the trademark, and the transaction should preserve enough continuity in products, services, quality, customer relationships, or brand reputation to support that transfer.

Goodwill reflects the total premium paid for a previously successful company after accounting for identifiable assets. Intangible assets other than the goodwill, such as patents, trademarks, software, and trade names, may be separately identifiable and separately valued (e.g., through the monetary value of an intellectual property license). The key difference is that goodwill usually represents the broader expectation that customers will continue doing business with the company, while other intangible assets may be specific assets with their own measurable value, legal rights, or limited useful life.

The Supreme Court addressed this distinction in Newark Morning Ledger Co. v. United States, 507 U.S. 546 (1993). In that case, The Herald Company purchased Booth Newspapers and allocated part of the purchase price to an intangible asset called “paid subscribers,” which represented the estimated future profits from identified newspaper subscribers existing at the time of the acquisition. The IRS disallowed depreciation deductions for that asset, arguing that the subscriber relationships were indistinguishable from goodwill because they reflected the expectation of continued customer patronage. The Court held that a taxpayer may treat a customer-based intangible asset as separate from goodwill if the taxpayer proves that the asset has an ascertainable value and a limited useful life that can be estimated with reasonable accuracy. The Court emphasized that the question is not simply whether the asset resembles goodwill, but whether it can be valued and whether that value diminishes over time.

The facts in Newark Morning Ledger illustrate why the line between business goodwill and other intangible assets can be difficult. A newspaper’s paid subscriber base obviously relates to customer loyalty and brand reputation, concepts commonly associated with goodwill. But the taxpayer showed that the acquired subscribers were a finite group, that subscriptions would be canceled over a predictable period, and that the asset was not self-regenerating in the way general goodwill can be. Because the paid subscriber asset could be identified, valued, and shown to waste over time, it was separable from goodwill for the tax issue before the Court.

That reasoning helps explain the relationship between goodwill and other intangible assets in a business sale. A buyer and seller may allocate value among trademarks, customer relationships, technology, tangible assets, and goodwill. Trademarks and trade names may reflect brand equity; customer contracts may reflect predictable future cash flows; software or proprietary technology may create operational advantages; and physical assets may have their own market value. After those identifiable assets and net identifiable assets are valued, the value of goodwill captures what remains: reputation, loyalty, workforce continuity, expected synergies, going-concern value, and the competitive advantage the buyer expects to inherit.

For business owners, the practical lesson is that goodwill is often the residual category, but it is not a dumping ground for every intangible value. If an asset can be specifically identified, separately valued, and tied to a finite useful life or legal right, it may be treated as one of the company’s other intangible assets rather than as goodwill. If the value instead comes from the company’s overall reputation, customer loyalty, assembled business, market position, or expectation of repeat business, that value is more likely to be treated as goodwill.

Goodwill impairment occurs when the fair value of the acquired business, reporting unit, or cash-generating unit falls below its "carrying value", which refers to the book value of an asset or reporting unit as shown on the company’s financial statements. In the goodwill context, the carrying value is important because accounting rules compare that recorded balance sheet value against the current fair value or recoverable value of the business unit to determine whether goodwill is overstated.

Impairment can result from reduced cash flow, increased competition, adverse economic conditions, loss of key customers, declining brand equity, regulatory change, or a drop in the market value of the acquired business. If those conditions reduce the expected value of the acquired business, the goodwill value recorded after the acquisition may no longer be supportable. The impairment reduces the goodwill account on the balance sheet and is recorded as an impairment expense on the income statement.

When goodwill is impaired, the impairment expense is recorded as a loss on the income statement and reduces net income. For public companies, that reduction can negatively affect earnings per share and the company’s stock price, particularly if the write-down signals that an acquisition failed to produce the future cash flows expected at the time of the acquisition.

The write-down also reduces the goodwill account on the balance sheet. This does not mean the company has less cash that day. It means the carrying value of the acquired goodwill no longer appears supportable.

Under generally accepted accounting principles (GAAP) and international financial reporting standards (IFRS), both public companies and private companies must evaluate goodwill reported on their financial statements and record impairments when the value of goodwill is no longer supported. This annual review helps prevent a goodwill account from remaining on the balance sheet at an inflated carrying value after an acquired business loses customers, market share, expected future cash flows, or brand reputation. For business owners, this matters because goodwill can increase reported assets, but it can also create later earnings volatility if the acquisition underperforms.

A related concept is negative goodwill, often described as a bargain purchase gain. Negative goodwill can occur when the purchase price paid for a target company is less than the fair value of the net assets acquired. In that situation, the acquiring company may recognize a gain because the buyer paid less than the identifiable net assets were worth.

Goodwill represents the premium a buyer pays above the fair market value of a company’s net assets. It is an intangible asset recorded on the acquiring company’s balance sheet, but it is not the same as a intellectual property asset or customer contract. Goodwill reflects brand reputation, customer loyalty, future cash flows, and the economic strength of an acquired business. The goodwill is closely tied to the company trademarks and branding because the trademarks are the symbols of that goodwill. The sale of a business comes with the value of goodwill.

If you need assistance with intellectual property matters, contact us for a free consultation.

© 2026 Sierra IP Law, PC. The information provided herein does not constitute legal advice, but merely conveys general information that may be beneficial to the public, and should not be viewed as a substitute for legal consultation in a particular case.

"Mark and William are stellar in the capabilities, work ethic, character, knowledge, responsiveness, and quality of work. Hubby and I are incredibly grateful for them as they've done a phenomenal job working tirelessly over a time span of at least five years on a series of patents for hubby. Grateful that Fresno has such amazing patent attorneys! They're second to none and they never disappoint. Thank you, Mark, William, and your entire team!!"

Linda Guzman

Sierra IP Law, PC - Patents, Trademarks & Copyrights

FRESNO

7030 N. Fruit Ave.

Suite 110

Fresno, CA 93711

(559) 436-3800 | phone

BAKERSFIELD

1925 G. Street

Bakersfield, CA 93301

(661) 200-7724 | phone

SAN LUIS OBISPO

956 Walnut Street, 2nd Floor

San Luis Obispo, CA 93401

(805) 275-0943 | phone

SACRAMENTO

180 Promenade Circle, Suite 300

Sacramento, CA 95834

(916) 209-8525 | phone

MODESTO

1300 10th St., Suite F.

Modesto, CA 95345

(209) 286-0069 | phone

SANTA BARBARA

414 Olive Street

Santa Barbara, CA 93101

(805) 275-0943 | phone

SAN MATEO

1650 Borel Place, Suite 216

San Mateo, CA, CA 94402

(650) 398-1644. | phone

STOCKTON

110 N. San Joaquin St., 2nd Floor

Stockton, CA 95202

(209) 286-0069 | phone

PORTLAND

425 NW 10th Ave., Suite 200

Portland, OR 97209

(503) 343-9983 | phone

TACOMA

1201 Pacific Avenue, Suite 600

Tacoma, WA 98402

(253) 345-1545 | phone

KENNEWICK

1030 N Center Pkwy Suite N196

Kennewick, WA 99336

(509) 255-3442 | phone

2023 Sierra IP Law, PC - Patents, Trademarks & Copyrights - All Rights Reserved - Sitemap Privacy Lawyer Fresno, CA - Trademark Lawyer Modesto CA - Patent Lawyer Bakersfield, CA - Trademark Lawyer Bakersfield, CA - Patent Lawyer San Luis Obispo, CA - Trademark Lawyer San Luis Obispo, CA - Trademark Infringement Lawyer Tacoma WA - Internet Lawyer Bakersfield, CA - Trademark Lawyer Sacramento, CA - Patent Lawyer Sacramento, CA - Trademark Infringement Lawyer Sacrament CA - Patent Lawyer Tacoma WA - Intellectual Property Lawyer Tacoma WA - Trademark lawyer Tacoma WA - Portland Patent Attorney - Santa Barbara Patent Attorney - Santa Barbara Trademark Attorney